Diversification is key for any passive investor and investing in different asset classes is an excellent way to diversify even further - but it often comes often at a price: if your portfolio is 100% equity based, adding other asset classes will likely reduce the overall return (because other asset classes are likely to give lower returns than equity). Therefore, diversification makes sense when the other asset classes are not correlated with equity - otherwise you are leaving money on the table (lower overall return) with no real benefit (no increase in diversification).

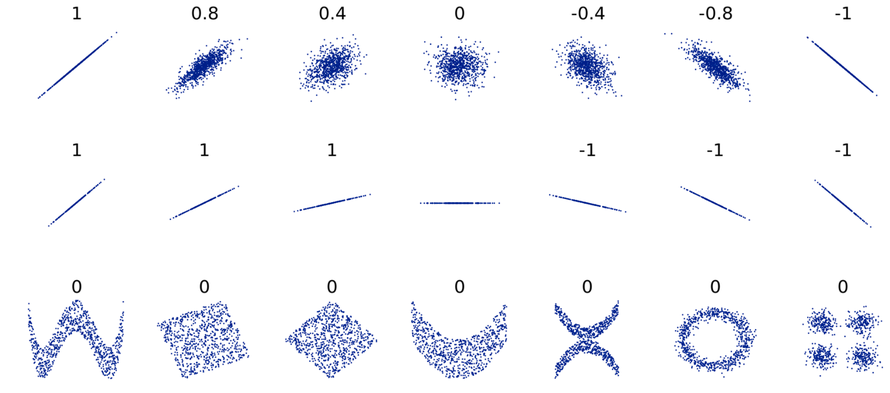

Wait, what do you mean by correlated? Correlation measures the degree to which 2 variables are (linearly) related to each other and its coefficient can vary between -1 and 1:

- If the correlation coefficient is -1, the 2 variables are perfectly correlated but they behave in an opposite way to each other. If one goes up, the other one will go down

- If the correlation coefficient is 0, the 2 variables are indipendent from each other - there is no linear relationship

- If the correlation coefficient is 1, the 2 variables are perfectly correlated and go in the same direction

Usually coefficients between 0.5 and 0.7 (plus or minus) indicate moderate correlation, while coefficients above 0.7 (plus or minus) indicates a strong correlation. From the Wikipedia page on correlation, I took this image which is a nice visual aid to understand the concept further:

So, the question at hand is - assuming I have currently a portfolio of equity (already well diversified), which other asset classes should I consider to diversify my portfolio? Let´s have a look at the correlations!

The data shown below is coming from the website www.portfoliovisualizer.com - specifically from this link and shows the correlation among ETFs "mimicking" different asset classes based on the monthly returns from January 2008 until January 2022.

You can read the table below as follows: IVV has a correlation coefficient of 0.9 with IJH and 0.1 with AGG.

I have tried to highlight some of the interesting clusters that emerge from this table:

- All Equity ETFs show a very strong correlation among each other. Personally I thought a different geographical focus would increase diversification quite a lot, but the correlation does not seem to point into this direction (that said, I would not change my base portfolio allocation)

- Bonds are indeed not correlated or (mildly) negatively correlated with equity ETFs. If we are looking to diversify our portfolio beyond equity, they are a prime candidate for that. Consider, though, the lower returns they offer. Corporate bonds are mildy correlated with equity, so going for government ones makes more sense in this context (focus on diversification). Bonds are also highly correlated among themselves so you can pick one and reap most of the diversification benefit.

- Investing in Real Estate ETFs (REIT = Real Estate Investment Trust) offers attractive returns, but the correlation with equity is quite strong, so the diversification benefit is limited

- Gold also offer good diversification potential as it is basically indipendent from equity

So, if you are looking for diversification on top of equity, bonds and gold are confirmed to be your best options. Real Estate ETFs and Commodities show higher level of correlation and therefore are less helpful in this sense.

If you want to learn more about different topics, click on the links below:

Write a comment