So far our discussion has been focused on investing for the long term. Our timeframe is often decades more than years. However, there are also cases where a shorter time span is needed.

Consider this scenario: I have 50K Euro and I need to reach 30K for the downpayment of a house. Getting the remaining 30K will take me probably 3 years.

What do I do with the 50K I already have today? One could argue to follow the same strategy we discussed in the previous posts - invest in (Equity) ETFs. However, 3 years is short time frame and if I need to pull out the money by then, we could be in the middle of a market dip that could have disastrous consequences for our investment.

Shall we leave them into the saving account? This is extremely safe of course, but inflation will eat up the value of our capital assuming your saving account does not offer any (meaningful) interest rate. Just to have a couple of numbers in mind, a 50K Euro capital after 3 years of inflation at 3% will be worth around 45.7K Euro in real terms - so you "lost" more than 4K Euro of purchase power.

What other options are available?

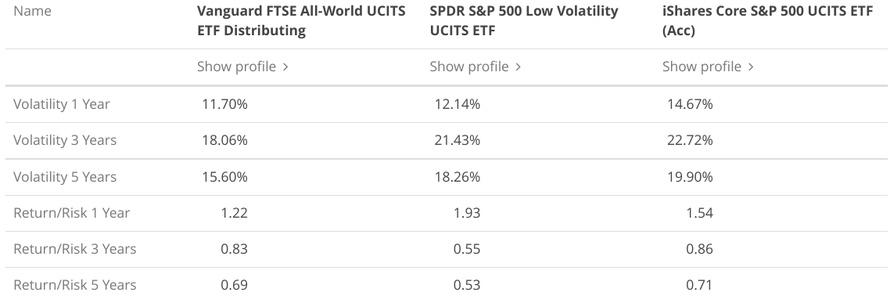

At first I thought about so called "low volatility" (equity) ETFs where basically the ETF is made up by the least volatile stocks in the reference market (e.g. S&P 500). However, there is only one above 100 mln Euro (remember, liquidity in this scenario is more important than ever) as of today and it tracks only the S&P 500. Moreover, when looking at its performance (below our Low volatility ETF is in the middle) and comparing it with the Vanguard All-World ETF and the normal S&P 500 I dont really see the benefits:

The Low volatility S&P 500 ETF seems to be indeed less volatile than the normal S&P 500 ETF - but the volatility of the All-World is even lower, so why should I bother with the Low Volatility one?

Another possibility is represented by Bonds ETF. The bond market in this period has a bit of tainted reputation because of very low returns but it provides (more) safety than investing in Equity. One important distinction is Corporate vs Government bonds. A Corporate bond is issued by a company (e.g. Nike), whereas a Government bond is issued by a country (e.g. Italy). As a rule of thumb, Corporate bonds offer higher returns than Government ones, as they need to offer a default risk and liquidity risk premium.

You know by now how to read the Factsheet of an Equity ETF but the Bond one is slightly different, so we will show an example here - iShares € High Yield Corp Bond ESG UCITS ETF EUR (Acc).

This is the key part and the terminology is different compared to an Equity ETF.

- Weighted Average Maturity is the average timespan before the main capital is paid back

- Weighted average Coupon is the annual payout you can expect to receive (based on the original face value)

- Weighted Average Yield to Maturity is the internal rate of return of the bond at the given market price. Basically, this is the interest rate at which all future expected cash flows are equal to the current price in the market to buy the bond.

- Effective Duration is maybe the more difficult concept to understand. Without going into details, it measures the sensitivity of the price of the bond to interest rate changes. In this specific case, if interest rates go up by 1%, the price is expected to drop by 3.49%. It is measured in years - not very intuitive I know (there are even different types of duration, Macaulay and Modified Duration but that is far too much for now)

Last but not least, in the description you should understand the Rating of the bonds included in the ETF. In this specific case, BB+ is the rating - which classifies these bonds as non-investment grade or "junk". The lower the rating (the best is AAA), the higher the risk of default and therefore the higher the return. You can find the full scale here.

In some cases, I heard about High Yield Saving Accounts - but not sure they are so popular here in Europe. The idea of some of them (fixed-term saving account) is that you put down a certain amount of money but cannot withdraw it until the term expires. Your return - though - is guaranteed and at the end of the term you will receive back the capital and the interests accrued.

I found this website that compares a few options in the market and it shows that if you have a capital of around 10K Euro you could get an interest rate up to 0.65% every year on that amount. Keep in mind in this case we end up talking about less than 200 Euro at the end of 3 years...

If you want to learn more about different topics, click on the links below:

- How to do your own spending review

- How much money do you need to reach your financial goal

- What is an ETF

- How to create a global ETF Portfolio with the least effort

- What is the Safe Withdrawal rate

- My Portfolio

- Lump sum vs Dollar Cost Averaging investing

- How to diversify your portfolio beyond equity

Write a comment